[Free Post] Harbor Diversified: A Potential Liquidation Play Trading Below Net Cash

How a struggling regional airline on OTC expert markets might be worth more dead than alive

Disclaimer: I own a few shares of Harbor Diversified, Inc., and stand to benefit if they rise in price. I may decide to purchase or sell shares at any time without prior notice. Do your own research and size positions appropriately if you invest. Nothing here is meant to be understood as investment or financial advice.

TL;DR

Harbor Diversified (HRBR), owner of Air Wisconsin, is a distressed OTC stock that appears to be trading below its liquidation value. After losing contracts with United and American Airlines, the company is "considering alternative strategies." With $104M in liquid assets against $46.7M in liabilities and additional non-liquid assets, an acquisition or liquidation could unlock significant value above the current $29.8M market cap. However, the stock trades on expert markets only with limited liquidity, the company has yet to catch up regarding its delayed filings, and management's plans remain unclear.

Introduction

This is a different kind of post than usual. It refers to a company that I bought a few shares of long before starting this blog. I now consider my decision-making process back then… “suboptimal”. As I was not too keen on spending too much time basking in my flawed decision-making of that time, I had Claude.ai help me with the editing and flow of the article. This article is free as I have not spent too much effort on writing it, and I believe it is difficult to act upon. In any circumstance, do additional research and apply an extra amount of caution. FYI, I won’t track this stock in the tracking page and probably never cover it again, either.

My Investment Misadventure

A couple of years back, I bought a few shares in Harbor Diversified (HRBR), owner of Air Wisconsin, a regional airline that operates by selling airflight capacity via purchase agreements to larger airlines. The stock was discussed on social media and YouTube, the assets seemed to cover the liabilities, and shares traded (what I thought) cheap on the OTC markets. In retrospect, I should have done more work analyzing the company before purchasing. Live and learn, I guess.

(Very Rough) Company Background & Recent Troubles

As far as my investment journey is concerned, HRBR's troubles began during COVID-19 when the company believed United owed them money for non-operated flights during the pandemic. HRBR lost the arbitration, causing a sizable amount of high-margin revenues to evaporate.

The subsequent timeline is telling:

The United capacity agreement was cancelled

HRBR struck a new agreement with American Airlines

The company fell behind on SEC filings

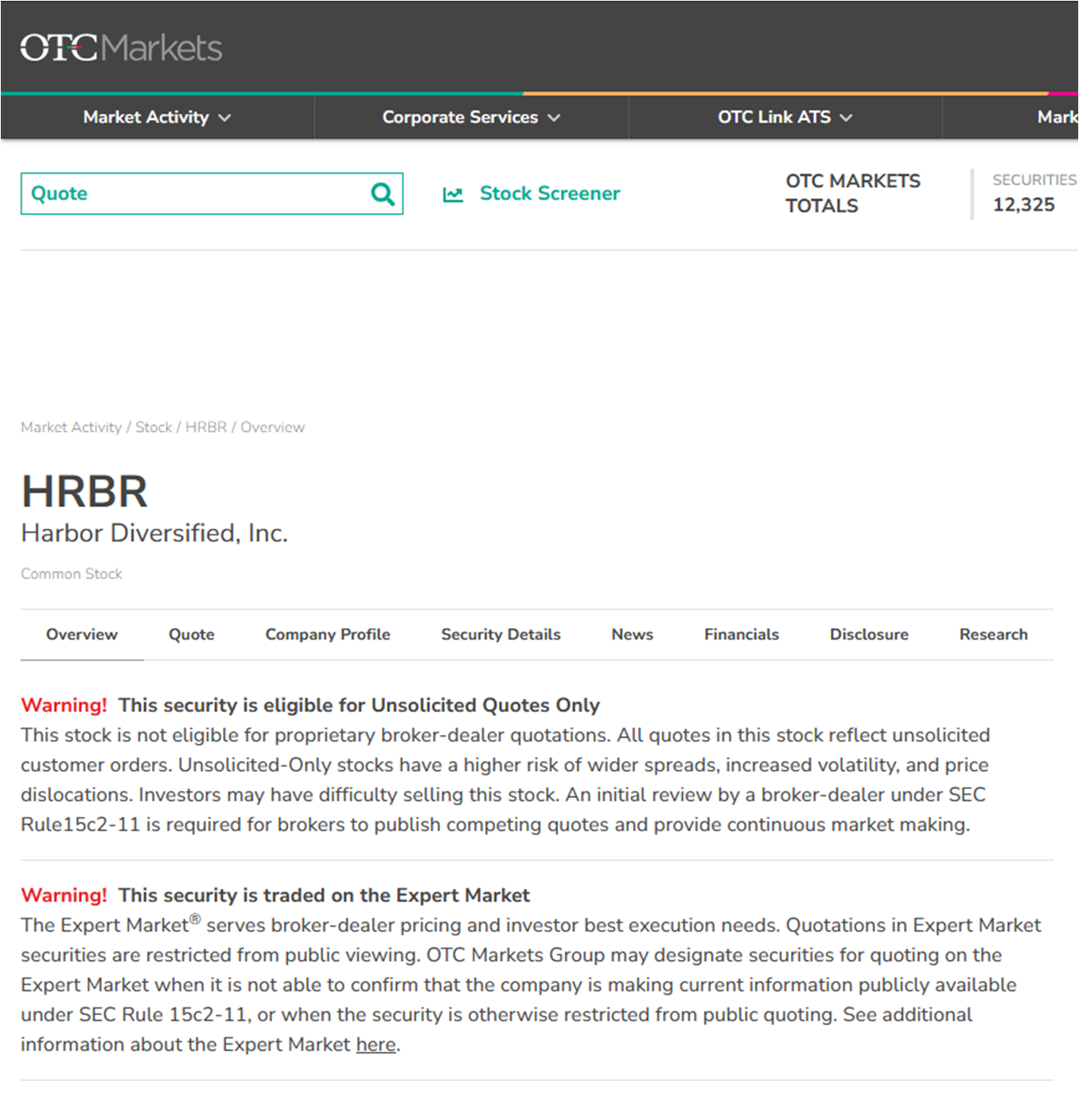

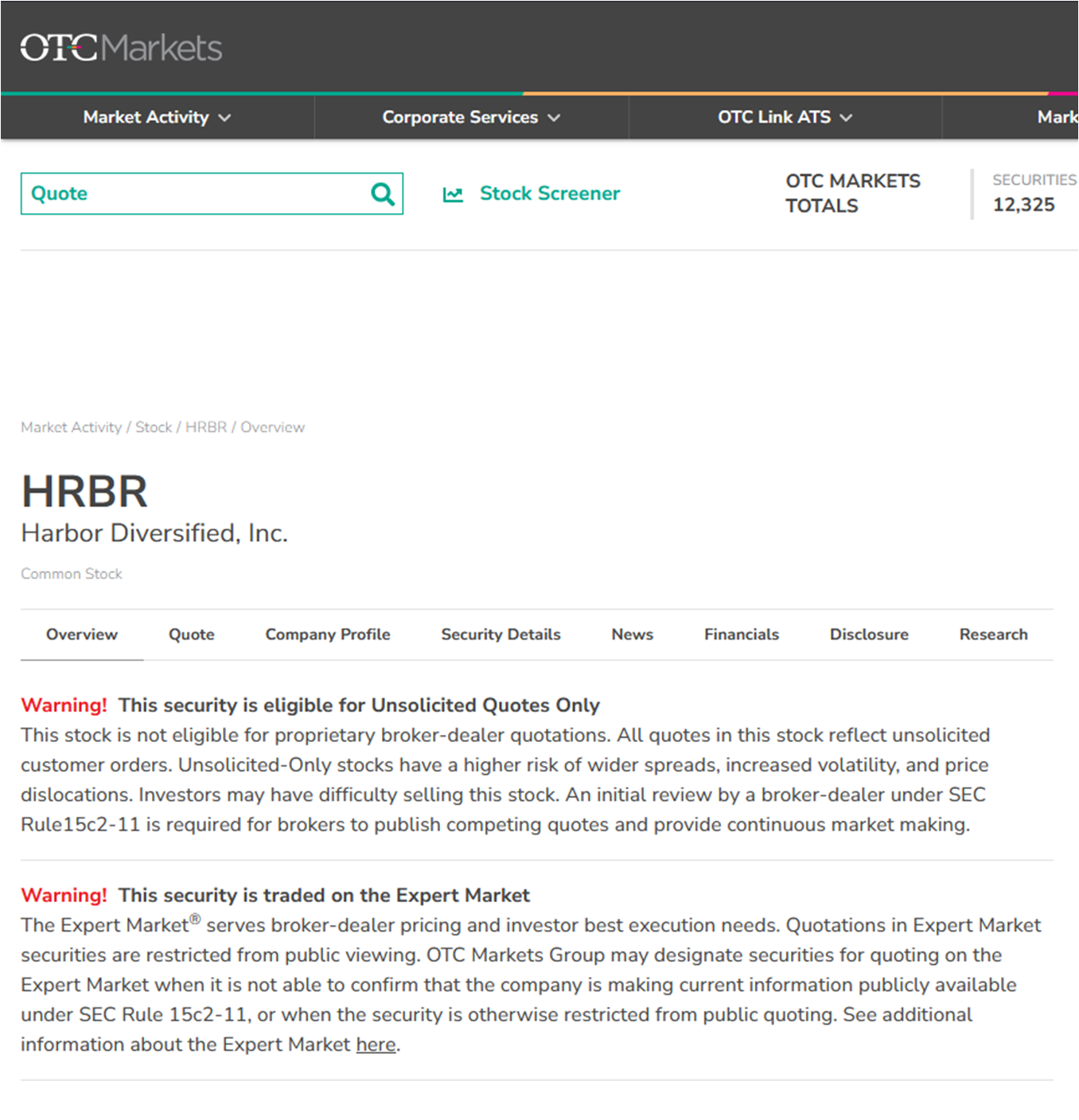

HRBR was downgraded to OTC expert markets only (meaning I can now only sell, not buy more shares through my broker)

At the beginning of 2025, the American capacity agreement was also cancelled

The company is now "continuing to evaluate the viability of these and other revenue-generating opportunities, while also considering alternative strategies".

Why This Stock Caught My Eye Again

Last Saturday, my long-forgotten Google alert indicated that HRBR filed its 10-Q for the quarter ending September 2024 (they're still behind on filings - case in point: the annual report for 2024 was announced as “not timely” the same day of the 10-Q filing). While reviewing the filing, I noticed some interesting details that make this a potential liquidation opportunity:

Simplified Capital Structure: In June 2024, the series C preferred stock was converted and redeemed. The company now has a clean capital stack with 58.4M common shares outstanding as of April 30, 2025.

Limited Cash Burn: The company lost money in the quarter, but not a lot. The net loss is small enough to be covered by D&A. A superficial look at the cash flow statement indicates positive FCF of $1M in the first 9 months of fiscal year 2024 (though be careful: accounts payable swung from -$5M in 2023 to +$5M in 2024).

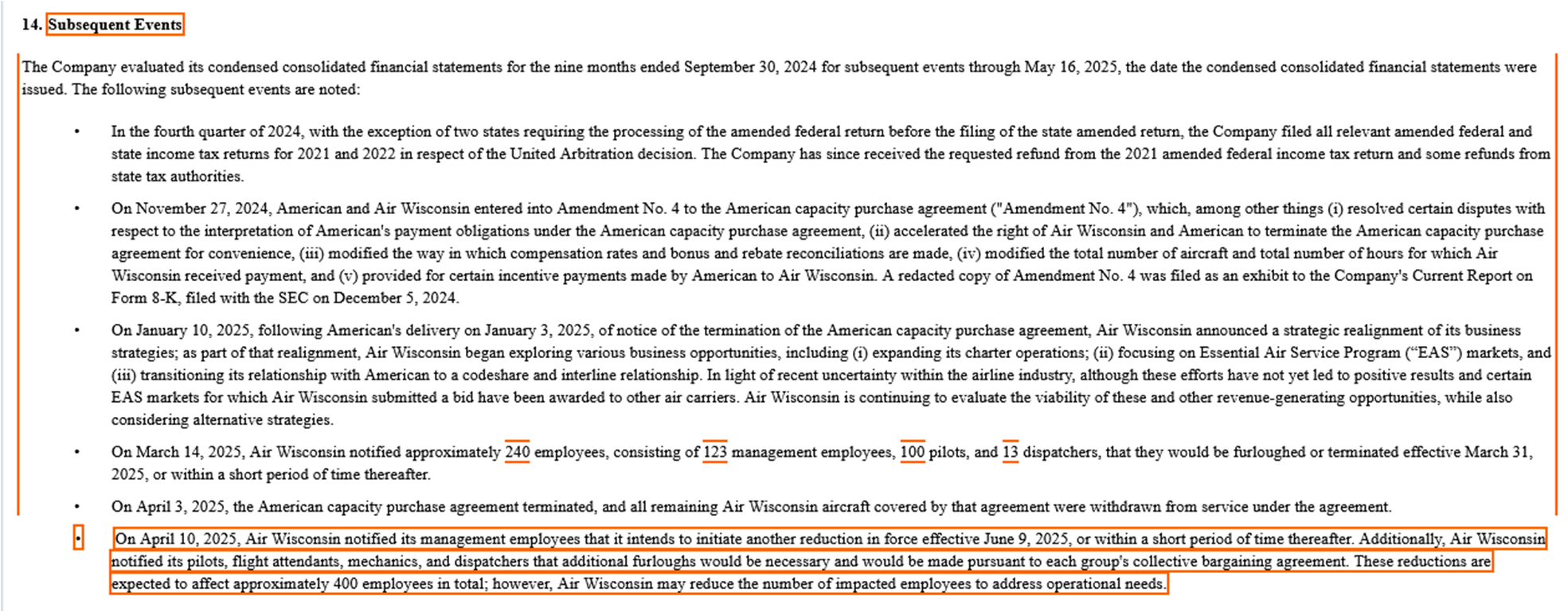

Cost-Cutting Measures: Based on the "subsequent events" section, the company is conserving cash by furloughing and potentially laying off staff while "considering alternative strategies."

The “subsequent events” section triggered me to write this brief article:

I take it that the company is conserving cash by furloughing and potentially laying off staff, it is attempting to generate revenue, but is also “considering alternative strategies”.

The Potential Liquidation Value

Yesterday’s (May 22, 2025) closing share price was $0.51, translating to a market capitalization of $27.9M with the 58.4M shares outstanding. But what would a liquidator or acquirer get?

Acquisition Cost:

$29.8M to acquire all shares

Potentially add a 20% control premium: ~$35.8M total

Asset Value:

$57.3M net liquid value (a $21.5M premium compared to the acquisition cost)

$104M in liquid assets

Minus $46.7M in liabilities

Additional Assets:

$100M in additional assets that you could fire-sell at a discount:

$50M in property & equipment value (planes and ground equipment)

$7M in current right-of-use assets

$6M in spare parts

$4.3M in receivables

$0.8M in restricted cash

$29M in long-term assets (investments, right of use,…)

Tax Benefits:

The company still has a retained deficit of $108M due to a series of losses

Significant NOLs (net operating loss carryforwards) could provide a valuable tax shield to an acquirer

Or maybe management goes another route and uses $100M in liquid assets to purchase something that generates operating income in the future. Who knows?

Some Key Risks to Consider

Market Access Issues: Mind the OTC markets warnings - shares are illiquid, difficult (if not impossible) to purchase, with wide spreads

Mind the OTC markets warnings, accessed May 17, 2025. Ongoing Losses: The company continues to operate at a loss

Outdated Information: Balance Sheet figures are as of September 2024, and the company is still not current with SEC filings

No Catalyst Timeline: No clear timeframe for the consideration of "alternative strategies"

Management Risk: Possible value-destructive M&A pursued by management

Insider Control: As of writing, 62.5% of shares are held by insiders, with no institutional ownership (according to Yahoo Finance)

{kind=link}

Conclusion

Harbor Diversified presents an interesting situation where the company appears to be worth significantly more than its current market price based on assets alone. While management hasn't explicitly announced liquidation plans, the "considering alternative strategies" language following the loss of their American Airlines contract suggests strategic options are being evaluated.

For investors who can access OTC expert market securities (which many retail investors cannot), this could represent an opportunity to purchase assets at a significant discount. However, without clear communication from management or a catalyst to unlock this value, it remains unclear when or if shareholders will benefit from the apparent asset-price disconnect.

Disclaimer

I own a few shares of Harbor Diversified, Inc., and stand to benefit if they rise in price. I may decide to purchase or sell shares at any time without prior notice. Do your own research and size positions appropriately if you invest. Nothing here is meant to be understood as investment or financial advice.

Would love to know your thoughts on today’s 8k!