Global Small- And Microcaps: A Second Source Of Alpha...

...by insulating against a certain type of systemic volatility risks.

Preamble: Many small- and microcap investors argue that due to the limited attention from analysts and institutions, they can gain alpha: outperformance by sifting through filings and identifying future winners earlier than the broader market. I subscribe to that view, but this article is about another type of alpha: the avoidance of a particular type of risk identified by Michael Green, brought about by the rise of so-called passive investing vehicles. I mentioned Green’s work in an article almost two years ago, and this article is my attempt to crystallize my thinking on whether the field I pursue provides a welcome protection. The thinking and writing were refined in collaboration with AI tools. The result is, I believe, a rational and consistent worldview, but I might be biased. If it prompts reflection or constructive feedback, I’d welcome it.

One Liner: The goal is not to avoid risk. It is to choose which risk you are willing to bear.

Executive Summary

The traditional model of the US equity market is approaching a structural threshold. As passive ownership approaches critical levels, the index’s ability to mean-revert to fundamental value weakens, replaced by a regime of heightened volatility driven by mechanical flows rather than economic signals.

This article summarizes my view on why quality microcaps and niche international equities offer a structural “exit” from this fragility. By operating in segments of the market that fall below the float and liquidity requirements of major index providers, these assets remain primarily priced by active participants. While this path trades systemic volatility for idiosyncratic liquidity risk, I argue that the ability to rely on distributable cash flows and active price discovery can act as a hedge against a “broken” (i.e. passive-dominated) large-cap ecosystem.

My core argument is simple: if passive investing increasingly weakens active price discovery in large-cap indices, then some of the most attractive long-term hunting grounds may be the parts of the market still dominated by active participants. Global small- and microcaps are not merely “less efficient.” They may increasingly represent a fundamentally different market structure — one where prices remain more tightly linked to business fundamentals than to mechanical capital flows.

Introduction

The ongoing debate over “Active vs. Passive” investing has shifted from a question of performance to one of market architecture. No longer are people simply changing their way of investing (and saving) by increasingly choosing passive over active vehicles, but, according to Michael Green, we are witnessing a change in how the market itself functions and what drives it: capital flows.

The following article is my attempt at rationalizing why I focus where I do, and it is intended to be read in conjunction with three main references: the recent working paper by Michael Green, Hari Krishnan, and Stephan Sturm, “A Model for Passive That Breaks the Market”; the market observations shared in the “Cocaine on the Tables” Substack article; and Michael Green’s recent interview regarding the structural limits of market insurance.

At 8th Wonder Capital, my focus is on international (including US) quality small- and microcaps. While often viewed through the lens of traditional “alpha seeking” (which was also my initial motivation), this article serves to articulate what I see as an additional benefit. It is an attempt to bridge the gap between the macro-fragility described by Green and the micro-level opportunities found in the “un-indexed” (or rather, “less-indexed”) corners of the market.

According to Green et al, we are moving into a regime where the largest, most liquid indices may ironically become the most unstable and “noisy” (in the sense that mechanical trading acts as noise obfuscating a value signal, feel free to challenge this perception), while the illiquid, overlooked “fundamental” stocks may provide a better, more reliable signal. This is not a “doomsday” thesis, but a critical systems analysis: when the primary engine of the market (the large-cap index) begins to override and dominate the laws of valuation due to mechanical supply and demand mechanics, the rational actor must look for an alternative engine.

While dominant buyer classes—from the 1920s retail speculators to 2008 central-bank liquidity—have always existed, the mechanical and price-insensitive nature of modern passive flows represents a qualitatively different shift in market self-correction.

Concepts: The Mechanics of Market Fragility

To understand why the “off-index” strategy is relevant, we must first address the specific mechanics of the fragility described by Green, Krishnan, and Sturm. Their model rests on the assumption that passive funds are, by definition, price-insensitive. They do not buy based on fundamental value (F); they buy or sell based on capital flows (p).

The Decay of Mean Reversion: In a healthy market, active investors act as “guard dogs,” going short overvalued assets and buying undervalued ones. This creates a force (k) that pulls the market price (S) back toward its fundamental value. Green’s paper demonstrates that as the passive share of the market increases, this pulling force weakens. Once passive ownership crosses approximately 65%, the market’s ability to correct itself diminishes, and at 90%, volatility begins to trend at “cubic speed”, according to the authors. The key point is not the exact mathematical exponent (“cubic”), but that volatility may accelerate nonlinearly once active price discovery falls below a critical threshold.

Author’s note: my understanding of mean reversion is around a different context: competitive dynamics and business cycles pull/push the margins and growth rates back towards the industry mean. This paper uses the fundamental value as a mean around which the market price fluctuates.The “Cocaine” Bid: As highlighted in the Cocaine on the Tables article referenced above, this is particularly visible in indices like the Russell 2000. These benchmarks can prop up “zombie” companies with deteriorating fundamentals simply because they are part of the basket that is bought by passive vehicles as investment capital flows into a corresponding passive vehicle. This “mechanical bid” functions like an artificial stimulant, masking potential balance sheet deteriorations.

The Insurance Gap: In his interviews, Michael Green points out a critical limitation for those attempting to hedge this risk. Structural “insurance”— I assume he speaks about long-dated Put options or LEAPS—typically only extends two years out. If the “passive break” is a multi-year demographic or structural shift, it becomes nearly impossible to hedge using traditional derivatives due to the prohibitive cost of carry and the rising counterparty risk of the market makers who sell these options.

The Structural Refuge: Off-Index and Off-Mainstream

If the primary source of risk is the “mechanical flow” into major indices, the logical solution is to seek assets that are structurally excluded from these flows.

Capital Density and Flow Impact

While niche ETFs exist for microcaps and specific international sectors, their absolute capital base is a rounding error compared to the trillions of dollars managed by Vanguard or BlackRock’s S&P 500 products. In these smaller segments, the “mechanical bid” is not strong enough to override the fundamental signal. Price discovery remains a function of active participants who are actually reading balance sheets, rather than algorithms executing 401(k) allocations.

Furthermore, the number of equities in the smaller Russell indices is much larger than, e.g., the NASDAQ 100, i.e., the smaller capital base (and flows) in the niche vehicles is spread over many more individual equities, which, even with a lower float and less trading, could dampen the flow effects. I have not seen empirical work quantifying this ‘flow dilution’ effect, but intuitively, the mechanism appears weaker when a smaller passive capital base is spread across thousands of securities rather than concentrated into a narrow mega-cap basket.

The Float Filter as an Insulation

One possibly counterintuitive protection for a microcap against volatility from passive vehicles is, ironically, its lack of trading liquidity. Most major index providers, such as S&P or MSCI, utilize Free-Float Adjusted Market Capitalization and strict liquidity thresholds for inclusion. If a company has a low float—perhaps due to concentrated founder ownership—it is structurally “un-indexable” for the larger indices, regardless of how well the business performs.

This “float filter” acts as an insulation from the mechanics that drive volatility. It prevents the passive machine from sucking the stock into its “cubic volatility” regime in the first place. By staying small and relatively illiquid, these companies remain in a “fundamental regime” where price and value are still tethered.

Admittedly, no microcap investor complains about the volatility on the way up. Therefore, I think that a microcap (with improving fundamentals) can actually use this to its investors’ advantage and exploit the reflexivity phenomenon: when fundamentals are improving, make capital structure decisions that support index uplisting/inclusion. This can serve to boost the share price due to the investment flows from passive vehicles, which then can actually help, e.g., raise additional funds to lower debt and capital costs.

International Insulation

Niche international markets, particularly those outside the US, often have significantly lower passive penetration. In many of these jurisdictions, the “Active Bid” is still the primary price setter. While these markets carry their own risks—such as geopolitical shifts or the exit of foreign capital—they are largely insulated from the specific US-centric passive “break” that Green describes.

The Capital Returns Buffer: Solvency in a “No-Trade” Regime

If the secondary market (the exchange) becomes unstable due to a passive collapse, liquidity may vanish entirely. In such a “no-trade” scenario, unless investors have a sufficient capital buffer, a primary return of capital can help investors ẉeather the storm.

This is why my focus is not just on “small”, sometimes illiquid stocks, but on Quality + Cash Flow. A company that pays a sustainable dividend or aggressively repurchases shares (maybe through tender offers) provides its own liquidity. If the market refuses to price the stock fairly, the company’s ability to return cash to shareholders (or buy out partners, which is what a share buyback does) becomes a transmission of value from business to investors, independent of index-driven volatility.

Author’s Note: If the structural refuge of microcaps seems too good to be true, it is because it comes with its own unique set of failure points…

The Reality of Systemic Risk: No Magic Bullets

While seeking refuge in the less-indexed corners of the market provides a structural shield against passive-induced volatility, it does not offer immunity. I currently see the following inherent risks in this “exit-the-passive” strategy.

Contagion and “Correlation to 1”: As Andy Constan has noted in recent discussions on bubble regimes and market contagion, structural breaks rarely remain localized. In a systemic liquidity event, i.e., when the stability criteria Green et al. discuss fail, the “Active Bid” in small- and microcaps may be overwhelmed not by passive flows, but by the necessity of active managers to raise cash. When the S&P 500 faces a margin-call-driven selloff, managers often sell what they can (liquid, high-quality microcaps) to protect what they must (their core large-cap positions). In these moments, correlations tend toward 1, regardless of fundamental divergence.

Similarly, as Constan describes, the late part of bubbles is characterized by low volatility and rising prices — a combination that encourages risk seeking and, e.g., levering up, which sows the seeds of demise and contagion through liquidation.The Liquidity Gap: From “Price Risk” to “No-Trade Risk”: In the large-cap world, the risk is usually that the price drops. In the microcap and niche international world, the risk is often that the market simply stops. During a period of “cubic volatility,” bid-ask spreads in illiquid names can widen to the point of absurdity. This is where the investment philosophy is tested: an investor must be psychologically and financially prepared for a “no-trade” regime where the quote on the screen is effectively meaningless.

Idiosyncratic vs. Systemic Risk: By moving off-index, the investor is intentionally trading Systemic Flow Risk (the risk of the machine breaking) for Idiosyncratic Business Risk (the risk of the company itself failing). Microcaps lack the “too big to fail” safety net and the diverse revenue streams of mega-caps. This strategy demands a much higher rigour in fundamental analysis; a structural refuge is only a refuge if the business within it is solvent.

The Regulatory and Institutional Variable: We must also consider the possibility of shifting rules. The institutions that have built empires on passive investing—and the regulatory frameworks that mandate 401(k) or Superannuation defaults—have a vested interest in preventing a “passive break.” As do public institutions. If flows were to reverse, it is possible we would see lobbying for “lock-in” mechanisms or changes to redemption rules. While intended to stabilize the system, such interventions could have the unintended consequence of further starving the small-cap ecosystem of active capital, making the “liquidity gap” even more pronounced.

We are Witnessing Real-Time Case Studies

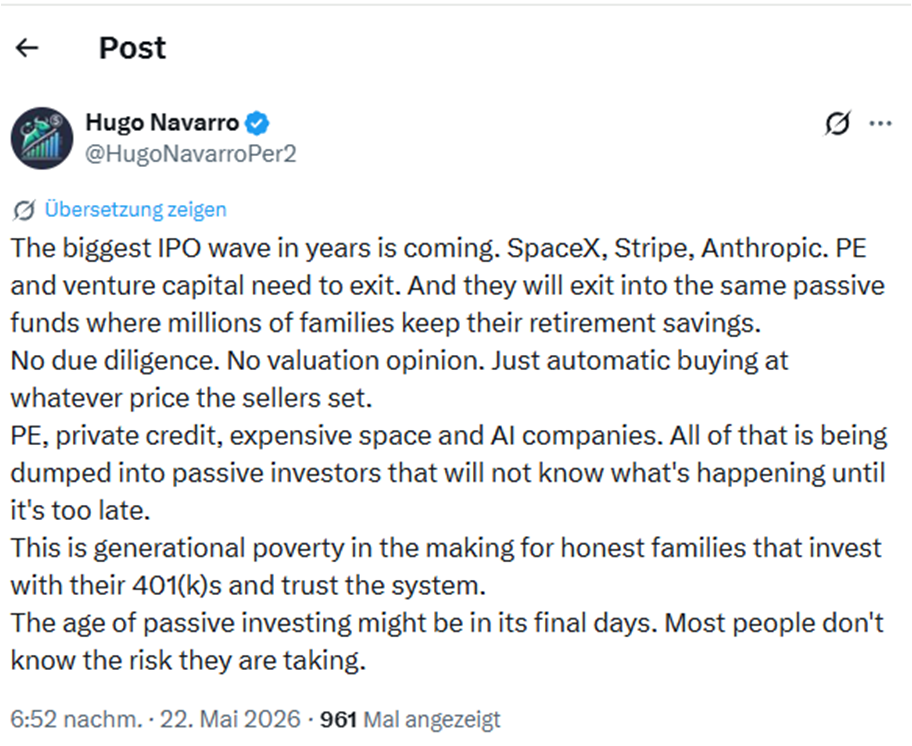

The following X-post by Hugo Navarro serves nicely to illustrate two timely points:

There can be real-world consequences and risks from passive flows. Without debating the merits or risks of the mentioned companies, they are without a long-term track record of profitability and can present heightened risk if they constitute a large part of the index (high valuation). Yes, they will see mechanical investment flows from passive vehicles, particularly upon index inclusion, but they can also see mechanical outflows. I would suspect, e.g., when lock-up periods end, or the volatility events predicted by Green et al, could ultimately lead to market panics and savers redeeming their funds, fueling the price-indiscriminate selling by passive vehicles, potentially impairing retirement savings vehicles.

It also helps to illustrate rule changes. Historically, a string of profitable quarters is needed for S&P 500 inclusion. However, S&P Dow Jones is reportedly considering rule changes to allow for faster index inclusion of mega IPOs: ”S&P Dow Jones Indices last week said in a proposal that it was consulting market participants about changing how mega-cap companies qualify into their indexes, defining "mega caps" as companies with market capitalizations equal to or greater than the 100th largest company in the S&P Total Market Index—which, at present, puts the threshold at around $110 billion.” Thus, irrespective of the merits of the space economy, many savers may not be aware that the passive vehicles they plan their retirement on will be significantly investing in a money-losing new IPO.

Conclusion: Choosing Your Risk

The goal of this article was to reason through and articulate my view on an aspect of investing that could present a veritable risk to investment returns. Ultimately, I see successful investing as coming in all forms and styles, one of which is global small- and microcaps. Beyond the potential for satisfactory returns, it appears to me that avoiding potential systemic volatility risk adds to this particular pond’s attractiveness, while it comes with other risks.

The Green, Krishnan, and Sturm paper provides a mathematical foundation for what many fundamental investors have felt intuitively: the link between price and value is fraying in the most “popular” segments of the market. If we accept that passive share is a parameter that weakens mean reversion, then I think one (of possibly many) logical responses is to seek out the areas where that parameter is lowest.

Focusing on quality (and this is important, however you defined quality), small- and microcaps and niche international equities is an attempt to stay in a market where the “guard dogs” are still awake. While not my initial underlying reason for why I invest in this corner of the market, it comes with an attractive property: prioritizing Fundamental Signal over Flow Momentum.

I recognize that by stepping outside the major indices, I exchange the “safety” of liquidity and the current “comfort” of the mechanical bid for a different set of challenges: higher idiosyncratic risk, more fragile businesses, and the potential for trading illiquidity. However, in a regime where the largest indices are suspected to be trending toward structural fragility, I view the ability to rely on a company’s independent cash flows and a human-driven price discovery process as a prudent form of insulation — and as sufficient for satisfactory returns.

On balance, I believe this view does not require a catastrophic “passive collapse” scenario to hold. Even if Green’s framework overstates the eventual instability, rising passive penetration may still incrementally weaken fundamental price discovery at the margin in the larger indices. If so, the relative attractiveness of less-indexed segments could increase well before any dramatic structural break occurs.

Importantly, “less indexed” does not automatically mean “more rational.” Many microcaps are dominated by promotional narratives, poor governance, limited disclosure, or retail speculation. My argument is narrower: that in sufficiently overlooked segments, active analysis still has a greater capacity to influence price discovery than in heavily indexed mega-cap ecosystems increasingly dominated by flow mechanics.

A final word on the term “risk”. You may have noticed that I, unlike I normally do, treated risk and volatility as interchangeable. Normally, I do not do so, as I perceive risk as the permanent impairment of capital (going out of business, or an impaired / misjudged earnings power going forward), and volatility as a source of opportunity (otherwise, how would I find undervalued companies?). However, in this article, I did not distinguish strictly for two reasons:

It would have made the article more cumbersome to read, and more importantly,

Volatility can constitute risk due to contagion effects, the reflexive impacts of volatility on the debt-liquidity cycle, and consumer sentiment impacts on the broader economy.

Appendix: 8th Wonder Capital Idea Inventory

For your reference, the following page contains a live-updated datawrapper table with links to the investment write-ups published on this substack. At the time of writing the respective articles, most ideas were well below $1b of market capitalization.

Global small and microcaps honestly feel like one of the few areas left where deep research still creates a real edge. Most people chase headlines while entire businesses quietly compound in the background. Really enjoyed this perspective.